Engineering and Mining Journal - Whether the market is copper, gold, nickel, iron ore, lead/zinc, PGM, diamonds or other commodities, E&MJ takes the lead in projecting trends, following development and reporting on the most efficient operating pr

Issue link: https://emj.epubxp.com/i/98266

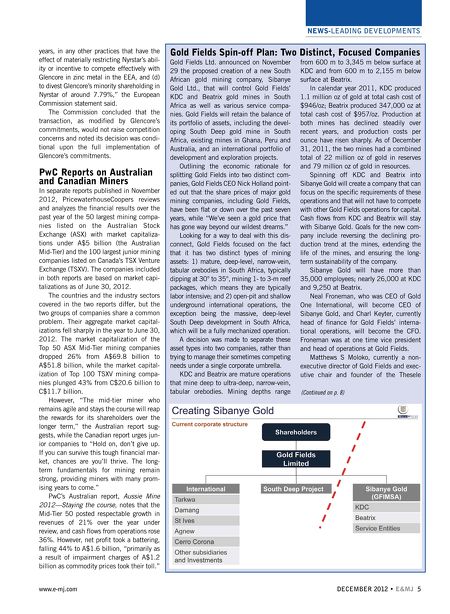

NEWS-LEADING DEVELOPMENTS Canada's Largest Gold Mine Nearing Production Glencore-Xstrata Merger Approved; Retention Package Rejected Detour Gold's new 55,000-mt/d mill includes two parallel comminution lines and conventional gravity and CIP gold-recovery circuits. (Photo courtesy of Detour Gold) Detour Gold began commissioning the first mill production line at its Detour Lake open-pit gold mine in northeastern Ontario in October 2012 and expects the first ore to be fed to the circuit before the end of the year. The first gold pour is scheduled for January 2013. When Detour Lake reaches design production rates in 2013, it will be Canada's largest gold mine. Gold production at Detour Lake during 2013 is expected to total between 350,000 and 400,000 oz. Life-of-mine gold production after full commissioning is scheduled to average 657,000 oz/y over a period of 21.5 years. Detour Lake currently has proven and probable open-pit mineral reserves of 15.6 million oz of gold in ore grading 1.03 g/mt at a cut-off grade of 0.5 g/mt. Once commercial production is declared, total cash costs are expected to be between $800 and $900/oz. As of the end of October 2012, Detour Gold had mined more than 20.3 million mt of material from the Detour Lake pit, with the majority of the material relating to prestripping. Approximately 1.1 million mt of ore had been stockpiled for future processing, which was in line with the company's plan of having 2.3 million mt of ore at an average grade of 0.81 g/mt by year-end 2012. The life-of-mine waste-to-ore strip ratio will be 3.6:1. 4 E&MJ; • DECEMBER 2012 Processing at Detour Lake will be through a conventional gravity and CIP plant. Two parallel lines will each have one secondary cone crusher, one SAG mill and one ball mill. At full production, mill throughput will total 55,000 mt/d. Pre-production capital costs for Detour Lake are expected to come in within 3% of the project cost estimate of C$1.45 billion, which dates from November 2011. As of September 30, 2012, Detour Gold had spent C$1.19 billion and had approximately C$348 million in cash and short-term investments, sufficient to fully finance the remaining project expenditures. Gerald Panneton, president and CEO of Detour Gold said, "We are now confident we will see the first ore in the mill circuit before year-end 2012, almost two months ahead of the original schedule. The first gold pour is expected to occur in January 2013 and will mark a new chapter in Detour Gold's successful history as it transitions from a developer to producer and becomes the next mid-tier gold producer in Canada." The Detour Lake mine is owned 100% by Detour Gold. The mine is located about 300 km northeast of Timmins, Ontario, and 185 km by road northeast of Cochrane, Ontario. The mine is located at the site of the former Detour Lake mine, an open-pit and underground mining operation that produced gold between 1983 and 1999. At meetings held on November 20, shareholders of Glencore International and Xstrata approved an all-share merger of the two companies, ending a tortuous process that began in February 2012 (E&MJ;, October 2012, p. 4). The merged company will be known as Glencore Xstrata plc and will have a market capitalization of about $85 billion. While approving the merger, Xstrata shareholders rejected a controversial $223million retention pay package designed to keep about 70 top Xstrata managers with the merged company. Xstrata Chairman Sir John Bond strongly supported the retention package, and when it failed, he said he would step down from his position as chairman of Glencore Xstrata plc once the company's board has completed a search for a new independent chairman. Xstrata Chief Executive Mick Davis will become CEO of Glencore Xstrata for a period of six months, after which Glencore CEO Ivan Glasenberg will take that position. The final merger transaction is based on Xstrata shareholders receiving 3.05 Glencore shares for each Xstrata share. The original proposed ratio was 2.8 to one and had been a sticking point for Xstrata shareholders, who felt it undervalued their shares. On November 22, two days after the shareholder approvals, the European Commission announced it cleared the acquisition of Xstrata by Glencore, conditional on the termination of Glencore's offtake arrangements for zinc metal in the European Economic Area (EEA) with Nyrstar and the divestiture of Glencore's minority shareholding in Nyrstar. The Commission had concerns that the merged entity would have the ability and incentive to raise prices for zinc metal. "To remove these concerns, Glencore committed (a) to terminate its exclusive long-term off-take agreement with Nyrstar, the largest European zinc metal producer, in so far as the agreement relates to commodity zinc products produced by Nyrstar in the EEA, (b) not to buy directly or indirectly any EEA zinc metal quantities from Nyrstar for a period of 10 years, (c) not to engage, for 10 www.e-mj.com